UK Watch: Stablecoins — When Regulation Becomes Payments Engineering

From statute and rulebooks to live settlement, redemption, and failure testing

Over the past year, the UK has produced an unusually dense sequence of cryptoasset and payments regulation. Read in isolation, these measures can appear incremental: a consultation paper here, a sandbox cohort there, a sprint framed as stakeholder engagement.

Read together, they reveal something more precise. Statute, supervisory rulebooks, sandbox evidence, and payments-infrastructure policy are now converging into a single regulatory system.

This note steps back to examine that system—not to ask whether stablecoins are permitted, but whether they can operate as payment instruments under supervisory stress.

Documenting a regulatory transition in real-time.

Regulatory position: the UK has entered the implementation phase

The UK has crossed a quiet but decisive threshold in stablecoin regulation.

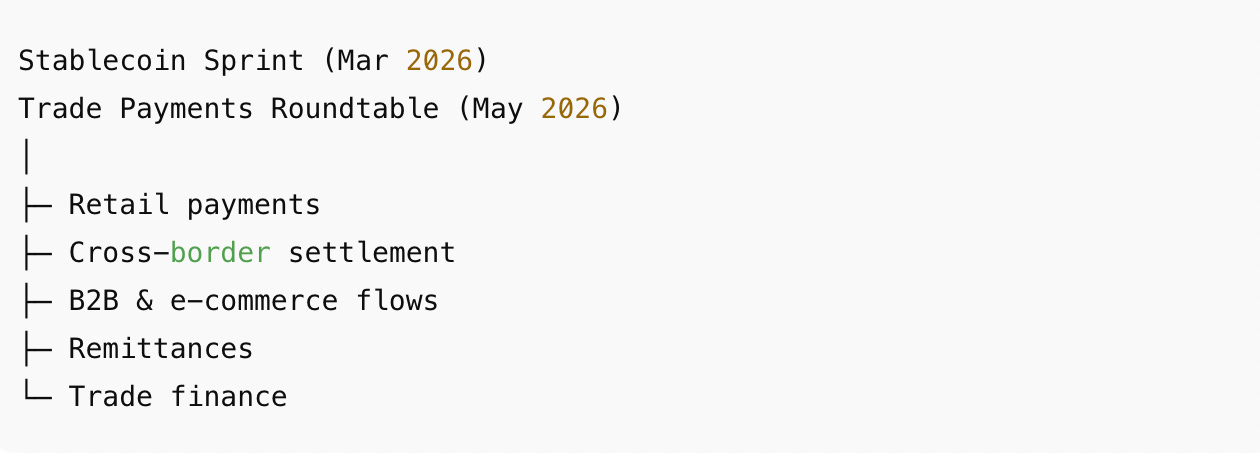

With the announcement of a Stablecoin Sprint (March 2026)1, a trade-payments roundtable (May 2026), and a dedicated stablecoins cohort inside the Regulatory Sandbox, the Financial Conduct Authority is no longer asking whether stablecoins belong in finance.

It is testing whether they function as money, as consultation closes and rulebook finalisation begins.

This reflects a transition from rule-writing to operational supervision, in which regulatory expectations are tested directly against live payment flows: regulation that compiles into infrastructure.

Why the current phase matters

Sprints and roundtables appear procedural. In regulatory sequencing, they are not.

Once a supervisor begins testing retail payments, cross-border flows, B2B settlement, remittances, and trade finance, the permissibility question has already been resolved. What remains is engineering discipline: whether instruments clear reliably, redeem at par under stress, and fail without propagating systemic harm.

That is the stage the UK has reached.

Regulatory sequencing — executed correctly

Financial infrastructure fails when legal clarity, supervisory expectations, and operational testing are misaligned. The UK avoided that failure by sequencing deliberately.

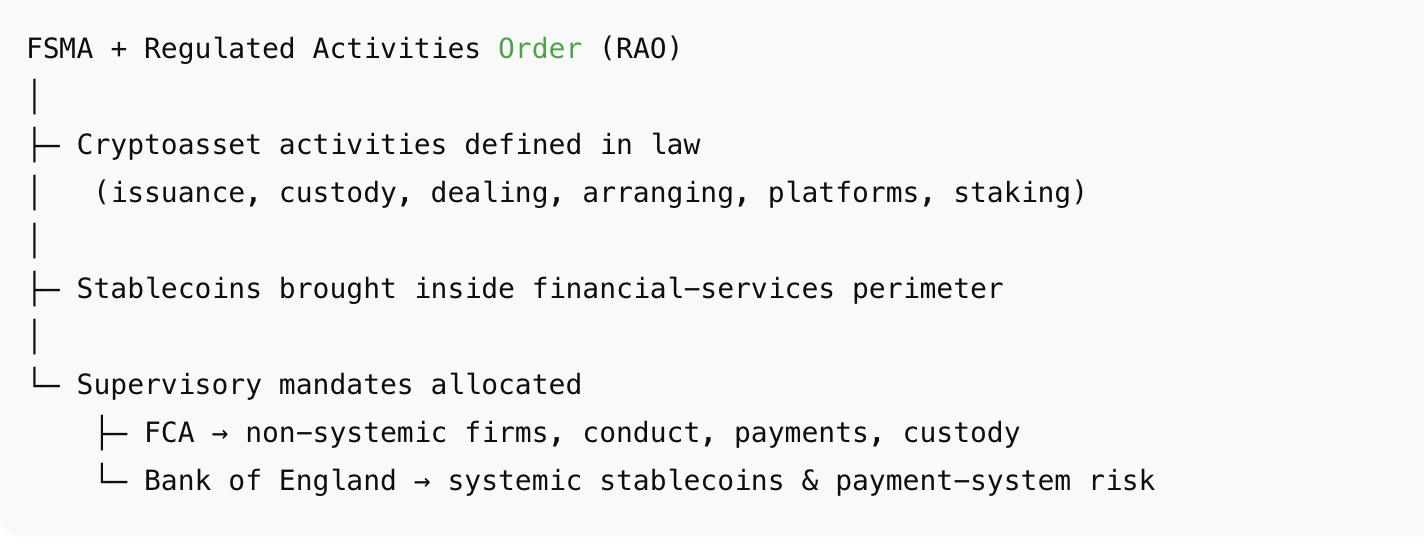

1) Perimeter first (law - FSMA / RAO)

HM Treasury amended the Regulated Activities Order under FSMA. Cryptoassets ceased to be a policy category and became defined regulated activities, each with an accountable supervisor.

Legal ambiguity ended at this stage.

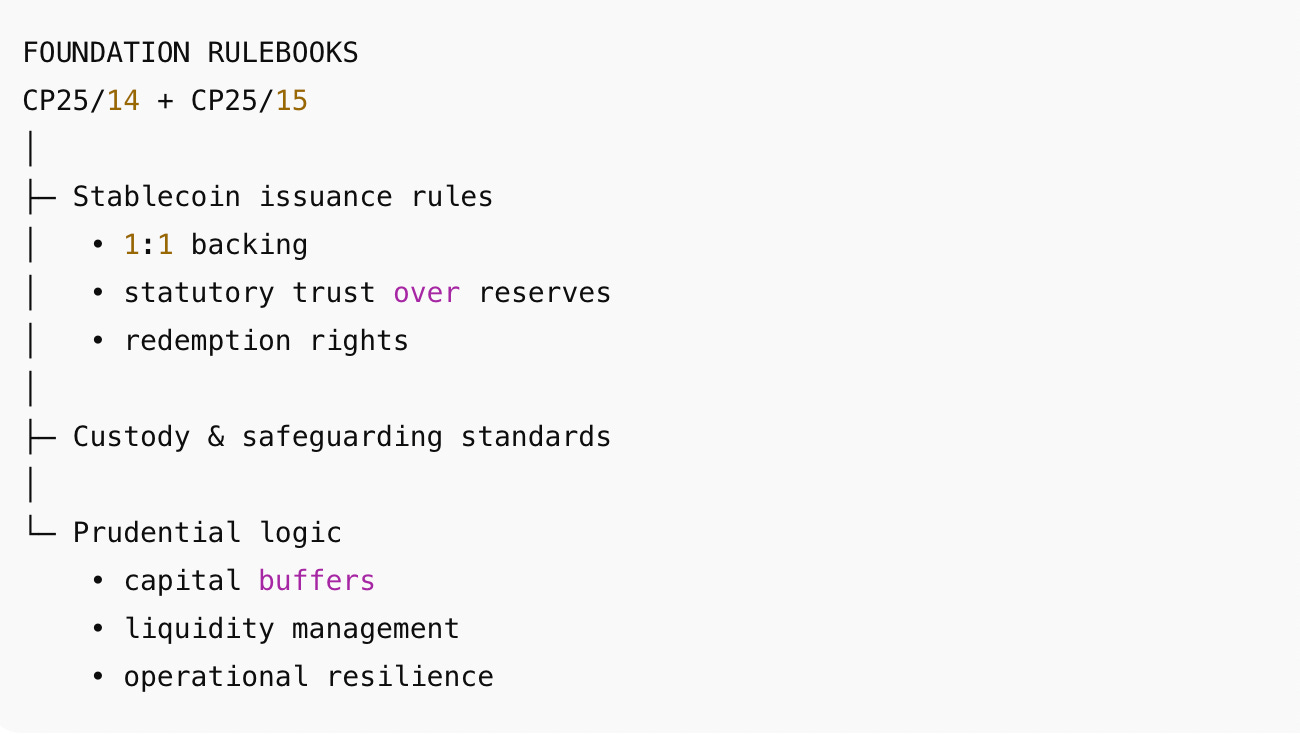

2) Obligations next (rulebooks - CP25/14 and CP25/15)

CP25/14 and CP25/15: these papers are the foundation of the UK stablecoin regime.

They translate statutory authority into enforceable requirements:

full reserve backing

statutory trust over backing assets

legally enforceable redemption rights

capital and liquidity buffers

governance, custody, and operational-resilience standards

Critically, the UK classified payment-focused stablecoins as payments infrastructure, not securities or investment products.

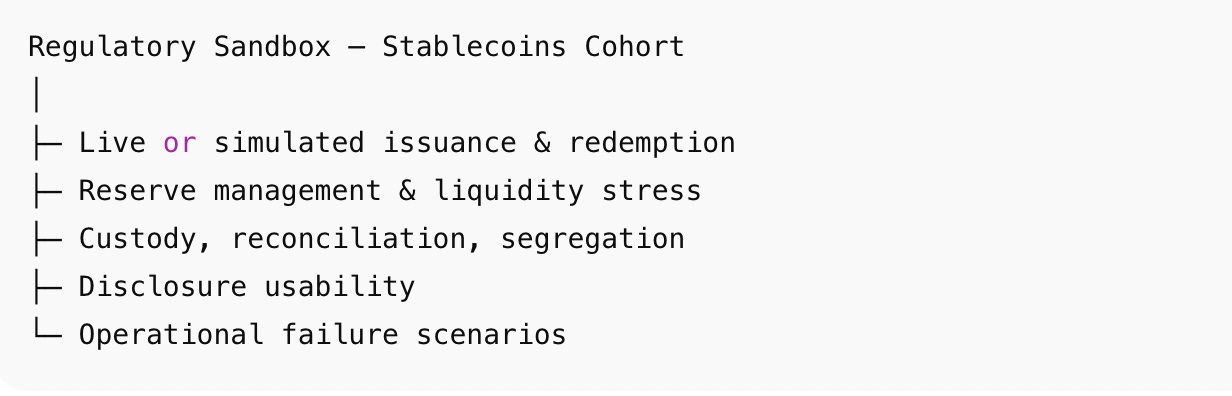

3) Supervisory evidence (Regulatory sandbox)

The FCA then opened a stablecoins cohort within its Sandbox. Firms are testing issuance, redemption, reserve management, custody, disclosures, and stress scenarios—often with live users.

This matters because sandbox findings directly inform final rules. Supervision is grounded in observed behaviour, not representations.

4) Synthesis (standards for payments)

The Stablecoin Sprint and trade-payments roundtable mark the synthesis phase.

These forums force CP25 obligations into real payment contexts: retail rails, cross-border settlement, B2B and trade flows. At this point, the regulatory test becomes operational:

Does this instrument clear, redeem, and fail safely at scale?

To make that sequencing explicit, the diagram below shows how the UK stablecoin regime progresses from statutory authority, to supervisory rulebooks, to live payments testing.

This is the regulatory logic now driving FCA action.

UK Stablecoins: Statutory → Supervisory → Operational Sequencing

How UK stablecoin regulation moves from law to live payment flows

This sequencing mirrors how the UK regulates other forms of critical financial infrastructure.

I. STATUTORY LAYER — Legal Authority

Who acts: HM Treasury → Parliament

What is decided: What is regulated, and under which legal powers

Policy function:

End ambiguity. Establish jurisdiction. Enable enforcement.

This layer answers whether regulation applies at all. Nothing operational happens without it.

II. SUPERVISORY LAYER — Rules & Expectations

Who acts: Financial Conduct Authority, Bank of England

What is decided: How regulated activity must be conducted

⬇ builds directly on this foundation ⬇

Policy function:

Translate statute into enforceable obligations. Align crypto with payments and prudential supervision.

CP25/40–42 do not replace CP25/14–15; they extend and operationalise them across the ecosystem.

III. SUPERVISORY EVIDENCE — Sandbox Testing

Who acts: FCA Innovation Hub

What is tested: Whether firms can comply in practice

Policy function:

Observe behaviour under controlled conditions. Identify failure modes before final rules.

Evidence gathered here feeds directly into supervisory calibration. This is pre-enforcement learning.

IV. OPERATIONAL LAYER — Payments Engineering

Who acts: FCA + industry + (where relevant) Bank of England

What is tested: Whether stablecoins function as money

Policy function:

Force legal and supervisory assumptions into real payment rails.

Regulatory test shifts to:

Does value clear at par?

Does redemption hold under stress?

Can failures be contained without systemic spillover?

At this stage, stablecoins are treated as payments infrastructure, not “crypto products”.

V. ESCALATION MECHANISM — Systemic Risk

Trigger: Scale + substitutability + criticality

Authority: Bank of England

Non-systemic → FCA-led supervision

Systemic relevance → BoE oversight

Policy function:

Contain systemic risk without suppressing early-stage innovation.

How the layers connect (one-line logic)

Statute defines scope → rulebooks define obligations → sandbox produces evidence → sprints set standards → systemic scale triggers central-bank oversight.

Why this sequencing matters

No leapfrogging from innovation to enforcement

No rule-writing without legal authority

No standards without observed behaviour

No systemic exposure without escalation capacity

This is regulation designed to compile into infrastructure.

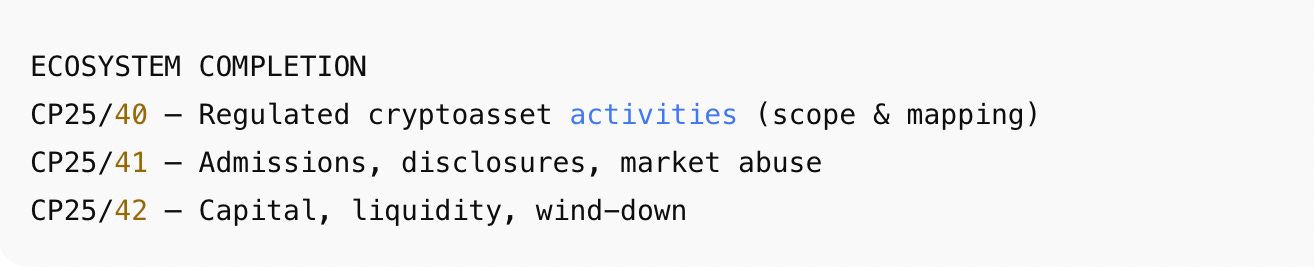

Why CP25/40–42 matter — and how they build on CP25/14–15

CP25/14–15 establish the core issuance and prudential obligations; CP25/40–42 extend and operationalise them across the wider ecosystem.

The payments-engineering phase is only possible because the FCA has already reinforced the supervisory stack above the CP25/14–15 foundation.

CP25/40 explicitly builds on those issuance and prudential baselines, completing the regulated activity map across trading venues, intermediaries, and custody.

CP25/41 standardises admissions, disclosures, and introduces a bespoke market-abuse regime.

CP25/42 embeds prudential expectations: capital adequacy, liquidity management, and orderly wind-down.

By the time standards are finalised, supervisory blind spots have already been reduced.

This is why the UK can move fast now. The scaffolding is already in place.

How the UK is treating stablecoins in practice

Strip away consultation language and the design philosophy is clear.

Stablecoins are treated as money-in-motion.

If an instrument settles payments at par, it belongs inside payments and financial-stability frameworks. Securities law would be the wrong tool for payment-focused stablecoins, which is why the UK has chosen payments regulation instead.Issuers face payments rules with bank-grade discipline.

Issuance is permitted—but only with full reserve backing, statutory trust structures, redemption rights, and prudential buffers calibrated to operational risk.Custody is treated as critical infrastructure.

Segregation, reconciliation, insolvency protection, operational resilience. Touch user funds, and you are inside the plumbing.Scale triggers escalation.

The Bank of England steps in when a stablecoin becomes systemically important, particularly where run risk and deposit substitution threaten bank funding stability. Innovation is tolerated at small scale; surprises are not tolerated at large scale.Evidence precedes enforcement: test first, standardise second.

Sandbox before enforcement. Evidence before final rules.

If you’ve followed The Future of Money, this arc has been visible for some time:

Perimeter → The UK Draws the Line on Crypto

Rulebooks → From Statute to Rulebook — CP25/14 & CP25/15

Regulatory posture → The FCA Doesn’t Want to Kill Crypto—It Just Wants to See It

Infrastructure design → Designing Money: Inside the UK’s Payments Blueprint

Comparative framework — Crypto Regulation in 2026: Where We Actually Stand

The UK’s Future Retail Payments Infrastructure strategy explicitly names regulated stablecoins, tokenised deposits, programmable payments, and AI-based integrity systems as technologies now safe to build with.

Regulation is no longer reacting to innovation. It is designing the rails innovation must run on.

What the UK is not doing

The UK is not banning stablecoins.

It is not classifying them as securities.

It is not relying on enforcement-first ambiguity.

It is not waiting for a retail CBDC.

It is not waiting for international coordination before moving forward—though it is designing with cross-border interoperability in mind.

Instead, it is integrating private payment instruments into public supervisory infrastructure—on clearly defined institutional terms.

It translates regulatory theory into concrete preparation tracks.

The FCA is no longer debating stablecoins—it is testing whether they clear, redeem, and fail safely inside real payment systems.

What follows

Up to this point, this issue has traced how the UK moved from statutory perimeter-setting to supervisory testing and payments-level synthesis.

What follows translates that architecture into regulatory readiness: the questions supervisors will implicitly ask, the artefacts firms will be expected to produce, and the failure modes that will matter once stablecoins touch live payment flows.

If you're preparing for Sandbox, Sprint, or authorisation, this is the implementation checklist:

→ **7 preparation tracks mapped to FCA supervisory expectations

→ **Required artefacts for each track (what to document, how to structure it)

→ **Timeline alignment (what’s needed before Sandbox, Sprint, final rules)

→ **Regulatory architecture mapping (which CP sections apply to which functions)

This is the operational layer most firms miss.

Groups that arrive with flows, controls, and evidence will shape the standards. Groups that arrive with narratives will inherit them.

* Consultation responses are due February 12, 2026.

* The Stablecoin Sprint runs March 2026.

* Policy statements expected mid-2026. Continue reading the complete operational framework: A Practical Checklist for UK Stablecoin Teams →